.webp)

The Components of Total Compensation

Base salary: the recurring foundation

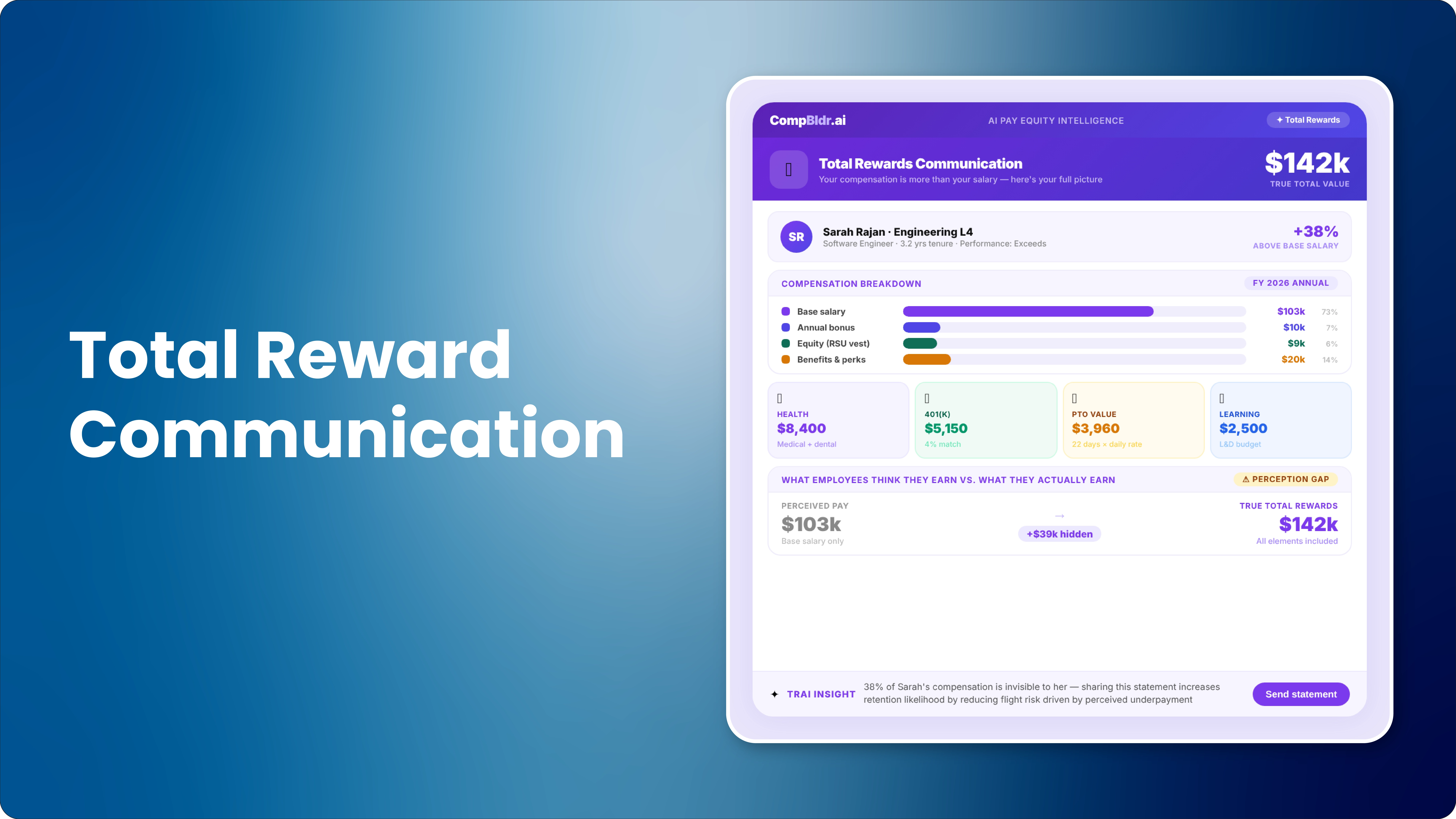

Base salary is the fixed annual pay an employee receives, typically paid bi-weekly or semi-monthly, that does not vary based on performance or company results. It is the most visible component of compensation and the one employees use most often when comparing offers. For most individual contributors and managers, base salary represents 70 to 90 percent of total cash compensation.

Short-term incentives: performance-based annual pay

Short-term incentives (STIs) include annual bonuses, sales commissions, and other performance-based payments that reset and are paid on an annual or more frequent cycle. They are designed to align individual or team behavior with near-term organizational goals. Target bonus percentages typically range from 5 to 15 percent of base salary for individual contributors and 20 to 50 percent or above for executive leadership.

Long-term incentives: equity and deferred value

Long-term incentives (LTIs) include equity grants such as restricted stock units (RSUs), stock options, and performance share units (PSUs), as well as deferred compensation plans. They are designed to align employees with long-term value creation and provide retention incentives through multi-year vesting schedules. For technology and executive roles, LTI value can exceed base salary as the largest component of total annual compensation.

Benefits: the often-undervalued component

Benefits include health insurance premiums paid by the employer, 401k or retirement contribution matching, life and disability insurance, paid time off, parental leave, and other employer-funded programs. Benefits are frequently undervalued in offer comparisons because they are less visible than cash compensation, but the employer cost of a comprehensive benefits package typically represents 20 to 35 percent of an employee's annual base salary.

Perquisites and additional compensation

Perquisites (perks) include company-provided items and allowances such as mobile phone stipends, home office allowances, transportation benefits, wellness stipends, professional development reimbursement, and company car programs. While individually modest, these can represent meaningful additional value and are increasingly used as differentiators in competitive hiring markets.

How to Calculate Total Compensation for a Role

Total cash compensation (TCC)

Total cash compensation includes only the cash components: base salary plus the target value of any short-term incentive. TCC = Annual Base Salary + (Target STI Percentage x Annual Base Salary). For a Software Engineer earning $130,000 base with a 10 percent target bonus, TCC = $130,000 + $13,000 = $143,000.

Total direct compensation (TDC)

Total direct compensation adds the annualized value of long-term incentive grants to TCC. TDC = TCC + Annualized LTI Value. If the same Software Engineer receives an RSU grant of $80,000 vesting over four years, the annualized LTI value is $20,000. TDC = $143,000 + $20,000 = $163,000.

Full total compensation

Full total compensation adds the employer-paid value of benefits to TDC. Full TC = TDC + Annualized Employer Benefit Costs. If the employer pays $18,000 annually in health insurance premiums and contributes $6,500 to the 401k, the benefit value is $24,500. Full TC = $163,000 + $24,500 = $187,500. This is the complete economic value the employee receives in a year.

Why Total Compensation Matters for HR Decisions

For competitive offer positioning

When a candidate compares your offer to a competing offer, they are (or should be) comparing full total compensation, not base salary alone. An organization that loses offers consistently on base salary may be winning on total compensation if equity, bonus, and benefits are competitive. Making total compensation visible and calculable in the offer process helps hiring managers have more effective conversations with candidates.

For pay equity analysis

Pay equity analysis that compares only base salaries can produce incomplete conclusions. If one demographic group receives lower base salaries but higher bonus targets or equity grants, a base-only analysis will overstate the equity gap. Conversely, if one group receives lower base salaries and lower equity grants, a base-only analysis will understate the true gap. Complete pay equity analysis should examine total cash and total direct compensation across protected groups.

For pay transparency compliance

Pay transparency laws in most US jurisdictions require disclosure of the salary or hourly wage range for a position. Some jurisdictions are beginning to expand this to require disclosure of bonus and benefit information. Regardless of what the law currently requires in your jurisdiction, being able to communicate total compensation clearly to candidates and employees positions your organization as a transparent employer and reduces pay-related attrition caused by perceived opacity.

Book a Demo See CompBldr in 15 minutes.

.webp)

.webp)

.svg)

.svg)

.svg)