.webp)

What Is the Difference Between a Market Adjustment and a Merit Increase?

A market adjustment is a salary change made to bring an employee's pay into alignment with the current external market rate for their role and grade, regardless of their performance rating. It corrects market lag. A merit increase is a salary change that rewards an employee's demonstrated performance during the most recent evaluation period. It recognizes contribution. Market adjustments are funded from a dedicated market correction budget, approved by Finance, and not subject to the merit matrix. Merit increases are funded from the annual merit budget, approved through the manager hierarchy, and governed by the merit matrix.

Why Running Both From the Same Budget Pool Creates Chaos

The structural problem with running market adjustments and merit increases from a single budget pool is not that organizations lack the intent to handle them separately. It is that most compensation platforms and spreadsheet-based cycle processes do not enforce the separation, so it gradually collapses under the pressure of a live cycle.

The merit matrix stops working when market adjustments are mixed in

A merit matrix recommends a merit increase percentage range based on two inputs: performance rating and compa-ratio (the employee's salary relative to the band midpoint). The matrix is calibrated to the total merit budget. If a manager submits a combined increase that includes both a market correction and a merit component through the same budget line, the merit matrix calculation is wrong for two reasons: the compa-ratio input uses the pre-adjustment salary (understating how competitive the employee's pay is), and the budget consumption includes adjustment dollars that were never part of the merit budget. The matrix loses its calibration.

Finance loses visibility into true merit spend.

Finance approves a merit budget based on compensation philosophy and headcount cost projections. If market adjustment dollars are booked against the merit budget line, Finance's view of merit spend is inflated. When the CHRO reports merit cycle outcomes to the board, the average merit increase percentage, percentage of employees at each performance tier who received increases at, above, or below the matrix range, those numbers include market correction spend that does not reflect merit differentiation. The reporting is wrong, the trend analysis from year to year is wrong, and Finance's ability to project future merit budgets is wrong.

Employees receive the wrong signal about why their pay changed.

An employee whose total increase was 6.5% but whose merit-only increase would have been 2.5% receives a 6.5% number without the context of what drove it. If the employee believes the full 6.5% reflects their performance rating, they hold an inflated expectation about future merit increases based on similar performance. When the following year's cycle produces a 2.8% increase for the same performance rating, the employee perceives a pay cut in real terms and a failure of the merit system, when in fact the merit system produced a consistent result, and the difference is that no market correction was needed. Employee trust in the compensation system is damaged by the communication failure, not by the actual pay decision.

The Dual-Budget Architecture: How to Separate the Pools Before the Cycle Opens

The dual-budget architecture is the governance decision made before the cycle opens, not a workflow adjustment made mid-cycle. It requires three things: defining the market adjustment pool separately from the merit pool, securing separate Finance authorization for each, and configuring the compensation system to track each pool independently.

Pool 1: The market adjustment budget

The market adjustment pool is sized by identifying every employee whose current salary is below a defined market competitiveness threshold, typically 90% of the current band midpoint for their grade, and calculating the cost of bringing each of those employees to the threshold. This is a defensible, bounded calculation: it does not grow or shrink based on performance rating, manager judgment, or discretionary considerations. The total cost of all threshold corrections in the eligible population is the market adjustment budget request presented to Finance. Finance approves a specific dollar amount for market corrections, separate from and before the merit budget is established.

The market adjustment pool is not a general-purpose correction fund. It exists specifically for employees who are below the competitiveness threshold as defined by the current salary band midpoints derived from updated survey data. An employee at 95% compa-ratio who has been with the organization for five years and whose manager believes they deserve a correction above the merit budget is not eligible for a market adjustment unless the data shows they are below threshold. Market adjustments are data-driven, not judgment-driven.

Pool 2: The merit increase budget

The merit increase budget is sized as a percentage of eligible payroll, typically 3% to 4.5% for US organizations in 2026, applied only to the eligible merit population. The eligible merit population is calculated after market adjustment eligibility has been determined: an employee who receives a market adjustment may still be eligible for a merit increase, but the merit increase is calculated on the post-adjustment salary, not the pre-adjustment salary. This distinction is important for budget sizing: if the merit pool is sized as a percentage of total payroll and the market adjustment population is large, sizing the merit pool before adjustments are applied will overstate the merit budget slightly.

The merit pool is distributed through the merit matrix: recommended increase ranges based on performance rating and compa-ratio zone, applied consistently across the eligible population by managers and reviewed by HR before approval.

How to size each pool before the cycle opens

The sequence matters: size the market adjustment pool first, then size the merit pool on the post-adjustment salary base.

The market adjustment pool sizing steps are:

- Pull the current compa-ratio for every employee in the eligible population.

- Filter for employees below the defined threshold, typically 0.90.

- Calculate the incremental cost to bring each to the threshold.

- Sum to the total market adjustment pool request.

The merit pool sizing steps are:

- Apply the market adjustments to the eligible employee salary base.

- Multiply the post-adjustment salary base for eligible merit employees by the target merit budget percentage.

- This is the merit pool dollar amount to request from Finance.

.webp)

Who Is Eligible for a Market Adjustment vs a Merit Increase

Eligibility criteria must be documented and applied consistently. Any discretionary eligibility determination creates the same governance problem as running both actions from a single budget pool: the process becomes subject to manager influence rather than data-driven criteria.

Market adjustment eligibility criteria

Standard market adjustment eligibility criteria:

- Compa-ratio below threshold: The employee's current salary is below the defined market competitiveness threshold (typically 90% of the current band midpoint based on updated survey data).

- Active employment status: The employee is actively employed in good standing at the time the cycle runs. Employees on performance improvement plans are typically excluded from market adjustments, though this is an organizational policy decision.

- No pending role change: The employee is not currently being processed for a promotion or grade change that would move them to a new band with a new midpoint. Market adjustments should not be applied to employees whose grade is about to change.

- Minimum tenure: Most organizations apply a minimum tenure requirement for market adjustments (typically 6 months in the current role) to avoid applying a market correction to an employee who was hired at a competitive salary that has not yet been tested in a merit cycle.

Merit increase eligibility criteria

Standard merit increase eligibility criteria:

- Performance rating: The employee received a performance rating in the most recent evaluation period. Employees without a current performance rating cannot receive a merit increase because there is no documented basis for the increase amount. The exception is new hires who have not yet completed a full evaluation cycle, who are typically excluded from the merit cycle in their first year.

- Minimum evaluation period: The employee must have been in their current role for a defined minimum period before the cycle close date, typically six to twelve months, to have a meaningful evaluation period.

- Performance threshold: Many organizations exclude employees at the lowest performance rating tier (Does Not Meet Expectations or equivalent) from merit eligibility. The merit budget is a retention and reward mechanism for employees contributing at or above the expected level.

Employees eligible for both: the sequencing question

When an employee is eligible for both a market adjustment and a merit increase, the sequencing of the two actions matters for two reasons: the merit matrix input (compa-ratio) changes after the market adjustment is applied, and the merit increase dollar amount changes if it is calculated as a percentage of the post-adjustment salary versus the pre-adjustment salary.

The correct sequence is: apply the market adjustment first, recalculate the employee's compa-ratio based on the post-adjustment salary, then use the updated compa-ratio as the merit matrix input for the merit increase recommendation. This sequence ensures that the merit matrix recommendation reflects the employee's actual competitive position after the market correction, not the artificially low position before it. An employee who was at 87% compa-ratio before a market adjustment that brings them to 92% will receive a different merit matrix recommendation than if the matrix had used 87% as the input.

The Approval Workflow: Two Actions, Two Chains, One Cycle Window

Market adjustment approval path

Market adjustments are data-driven corrections, not manager proposals. The HR compensation team identifies eligible employees and calculates the adjustment amounts before the cycle opens. The approval chain is: HR compensation team generates the adjustment list based on eligibility criteria and pool size, HR Director or Total Rewards Director reviews and approves the list as a batch, Finance approves the total pool spend against the pre-authorized market adjustment budget, and the adjustments are applied without a manager-by-manager proposal. Managers are informed of market adjustments to their direct reports as a communication step, not as an approval step.

This is the critical structural distinction from merit increases. Managers do not propose market adjustments. If managers are involved in proposing market adjustments, the adjustment process becomes a second merit cycle with broader management discretion, which defeats the data-driven purpose of a market correction program.

Merit increase approval path

Merit increases follow the standard manager-led approval chain: managers propose increases for each direct report within the merit matrix recommended range, or outside the range with documented rationale, proposals route to the manager's manager for review, HR reviews the full population for merit matrix compliance and TrAI equity flag resolution, Finance reviews aggregate budget consumption, and final approval from the CHRO or compensation committee closes the cycle.

Why the two workflows must stay separate even when they run simultaneously

Running both workflows in the same cycle window is operationally efficient. But if the workflows share approval steps, the separation breaks down. A manager who can see and modify both the market adjustment and the merit proposal for their direct reports in the same interface will inevitably treat the market adjustment as an additional lever in the merit negotiation, which it is not. The market adjustment amount is determined by data. The merit increase amount is determined by performance and budget. Separating the interfaces and the approval chains enforces the conceptual separation that prevents the two pools from effectively merging into one.

How to Communicate Both Actions Without Confusing Employees

Single communication, two clearly labeled components

Employees receiving both a market adjustment and a merit increase should receive a single communication that presents both components with their separate rationales labeled explicitly. The communication might read: 'Your base salary is being adjusted in two separate actions effective [date]. A market adjustment of [dollar amount or percentage] reflects that the current market rate for your role and grade has increased relative to your current salary. This adjustment is separate from your performance rating and applies to all eligible employees whose salary falls below our market competitiveness threshold. A merit increase of [dollar amount or percentage] reflects your [performance rating] in the [evaluation period] cycle. This increase is governed by our merit matrix and reflects your individual contribution.'

This format is more complex than a single percentage. It is also more accurate, more defensible, and less likely to create wrong expectations about future cycles. An employee who understands that 4.1% of their total 6.6% increase was a market correction and 2.5% was their merit award does not expect 6.6% every year simply because their performance was consistent.

What managers should say and what they should not say

Managers communicating both actions should: explain the market adjustment as a data-driven correction applied to all eligible employees, explain the merit increase as an individual recognition of their specific performance, confirm the combined effective salary and the effective date of each action, and invite questions about either component. Managers should not: present the combined percentage as a single undifferentiated merit increase, imply that the market adjustment reflects any performance evaluation, or suggest that either component is subject to further negotiation.

The documentation that supports each action

Each action requires separate documentation: the market adjustment requires documentation of the employee's compa-ratio before the adjustment, the current band midpoint, the threshold that triggered eligibility, and the calculation method. The merit increase requires documentation of the performance rating, the merit matrix range for that rating and pre-adjustment compa-ratio zone, and the proposed amount relative to the matrix range. Both documents are stored permanently in CompBldr and are retrievable for pay equity audits, OFCCP examinations, or pay transparency disclosure requests.

.webp)

Common Mistakes That Turn a Dual-Action Cycle Into Budget Chaos

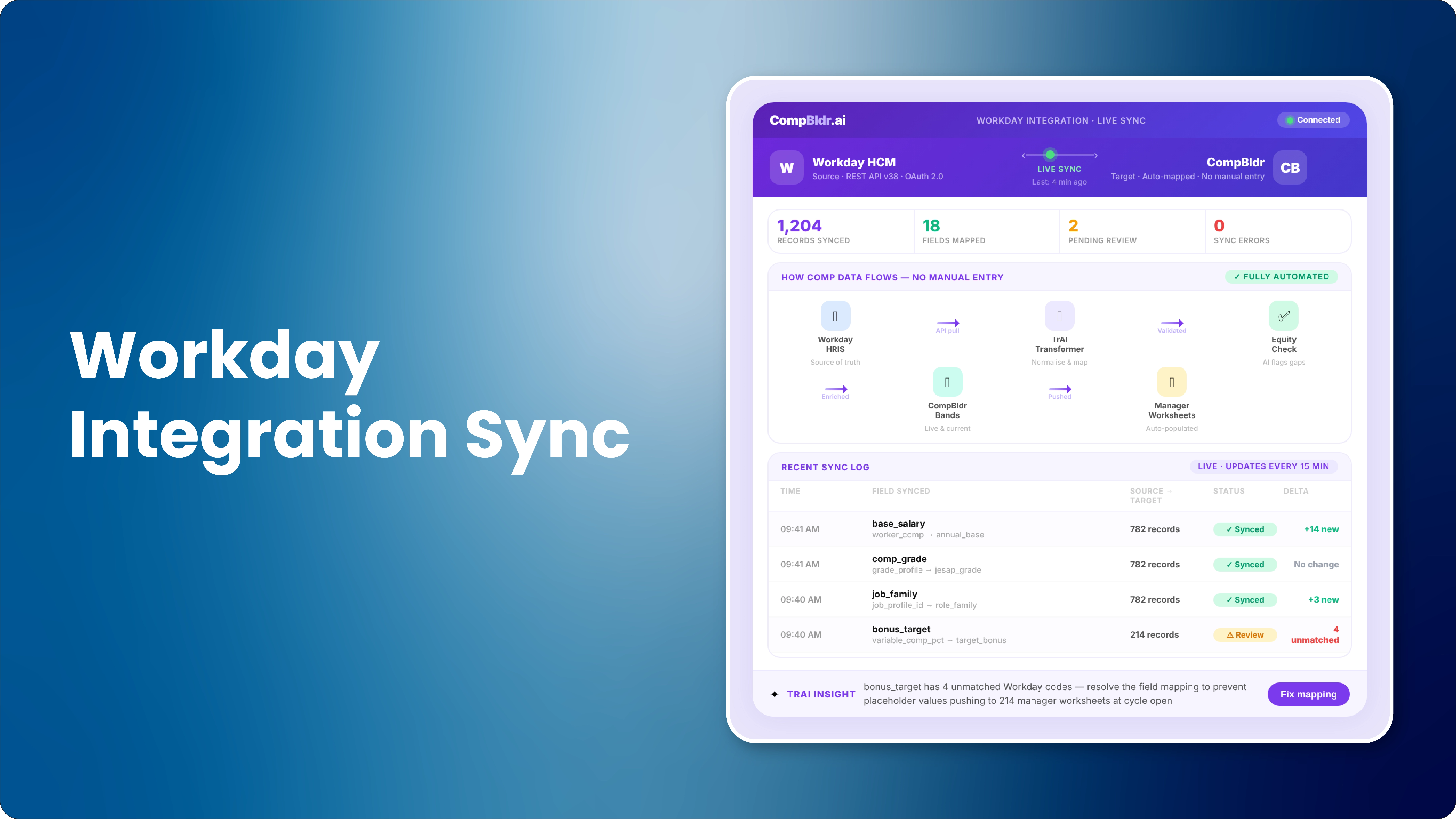

How CompBldr Manages Market Adjustments and Merit Increases in One Cycle

CompBldr's compensation planning module supports dual-pool cycle architecture as a configuration option rather than requiring HR to enforce the separation through manual process discipline. Before the cycle opens, the HR team configures two separate budget pools within the same cycle: the market adjustment pool with its eligibility criteria and Finance-approved dollar amount, and the merit pool with its merit matrix configuration and headcount-based percentage budget.

During the cycle, market adjustment proposals are generated by the system based on compa-ratio data and are routed directly to Finance and HR for batch approval, bypassing the manager workflow. Merit proposals are routed to managers who see their team's merit matrix recommended ranges pre-populated, the updated post-adjustment compa-ratio as the input, and real-time budget consumption for the merit pool. TrAI monitors both pools for equity patterns: the market adjustment pool for systematic gaps in which employee clusters are below the threshold, and the merit pool for the standard merit cycle equity signals.

At cycle close, CompBldr generates the employee communication template for employees receiving both actions, with each component labeled and the combined effective salary confirmed. Finance receives a cycle close summary showing actual spend against the approved budget for each pool separately. The compensation analytics dashboard updates with the post-cycle compa-ratio distribution reflecting both actions.

Market adjustments and merit increases answer different questions. A market adjustment answer: Is this employee paid competitively, given what the current market pays for this role? A merit increase answers: Did this employee perform in a way that merits recognition through a salary increase? The two questions have different answers for different employees, require different data inputs, draw from different budget pools, need different approval authorities, and produce different employee communications.

Running both in one compensation cycle is not only possible but common. Budget chaos is not an inevitable consequence of running both. It is a consequence of running both through the same pool, the same approval chain, the same communication template, and the same budget line. The dual-budget architecture prevents chaos by establishing the separation before the cycle opens, when changing it is straightforward, rather than trying to enforce it mid-cycle, when everything is live, and the pressure is already building.

.webp)

.svg)

.svg)

.svg)